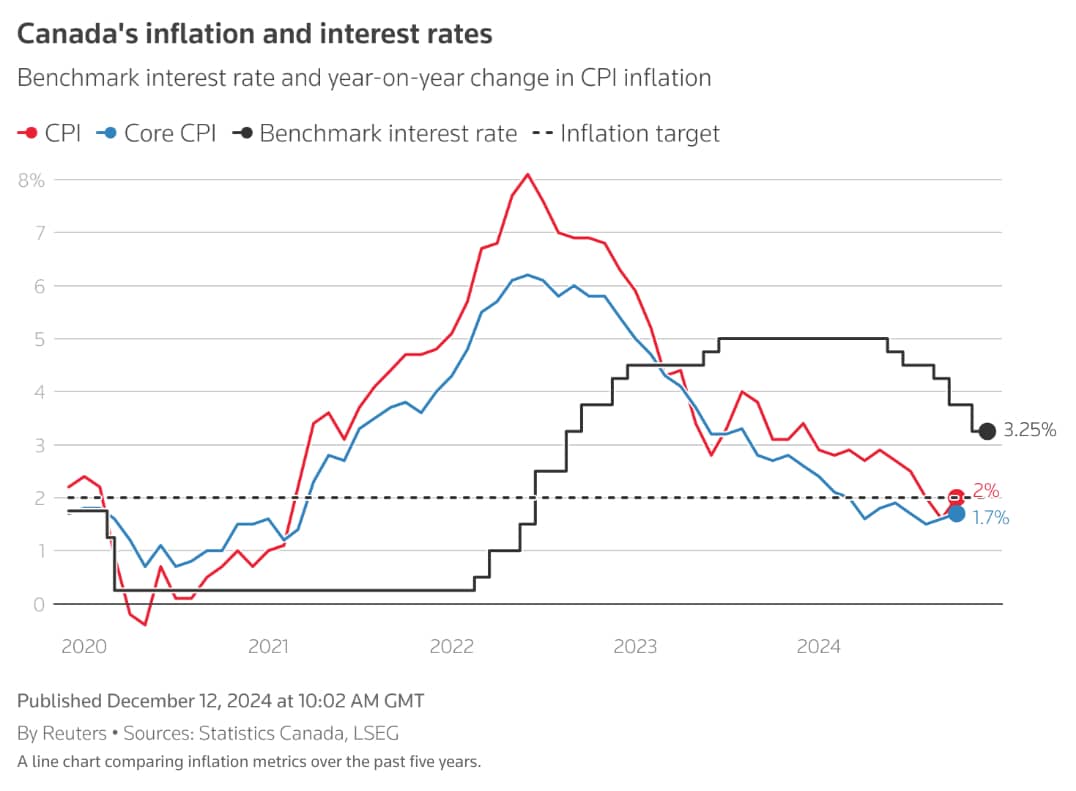

Yesterday, the Bank of Canada continued its interest rate cuts with another 0.5% decrease. BoC has cut rates a cumulative 1.75% this year.

Canada has aggressively cut interest rates compared to developed countries

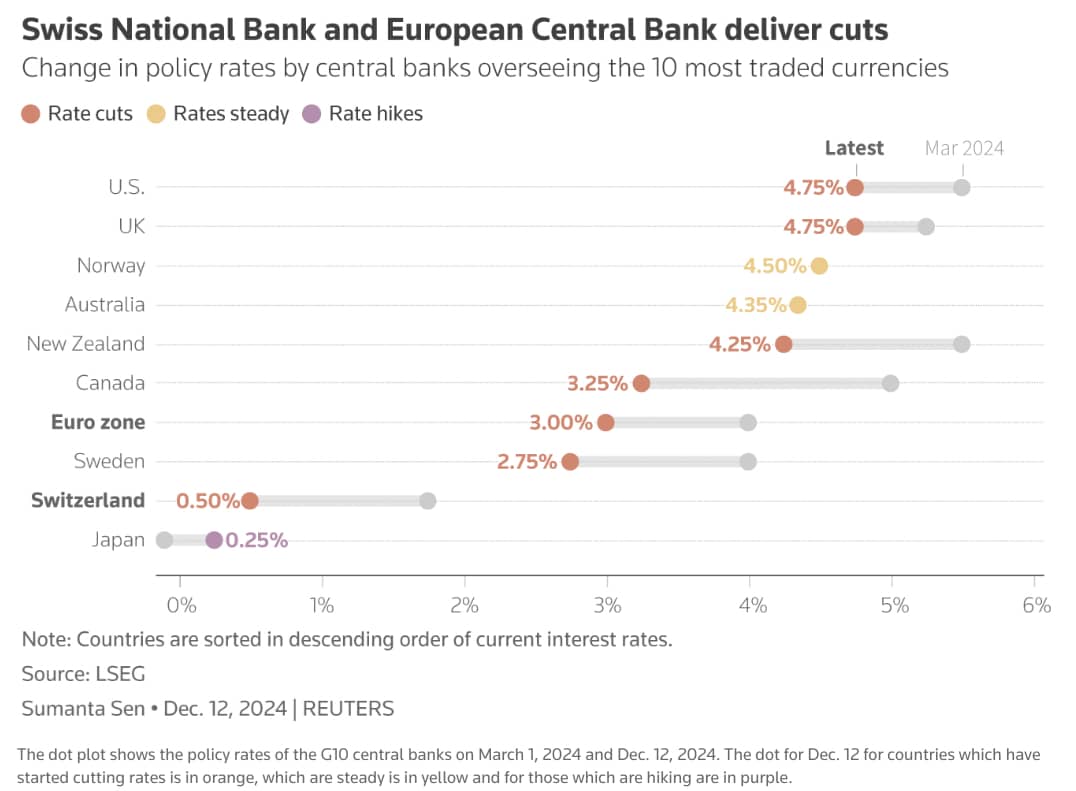

Reuters published a very informative comparison of rate decisions by central banks in major countries:

Canada’s underlying metrics are showing a weak economy. Our GDP per capita remains in decline. Anecdotally, I am seeing large corporations entering a cost-cutting phase, including layoffs. As consumers tighten their wallets, corporations will face limited revenue growth. Companies are preparing their P&Ls to weather a difficult upcoming year.

With inflation barely meeting the BoC’s 2% targets, I am encouraged that the BoC is taking a more proactive stance on cutting rates quickly.

I don’t currently see any catalyst to jumpstart the Canadian economy over the next year. With the potential US-Canada tariffs war to come in 2025, it adds further risk and uncertainty. I’d suspect further rate cuts to come in the new year. If tariffs are implemented on a wide and deep scale, I wouldn’t be surprised to see further BoC rate cuts of up to 1%.

Focus on what you can control

Since I have no control over the macro factors in the markets, I can only focus on what I can control: our savings plans and our mortgage repayment progress.

2021: We took a variable rate mortgage

In December 2021, we refinanced our mortgage to a lower rate, but kept to a variable rate mortgage. At Prime-1.19%, the variable rate at the time was 1.26%. We were also offered a fixed rate mortgage option around 2%, which we declined.

At the time, I thought that the Bank of Canada would slowly increase rates and that a variable rate mortgage would put us ahead. We were also prepared for the worst: rates had been at historical lows and rising rates should have been expected. When we went with a variable rate mortgage, we made sure we could absorb mortgage rates going back to its historical average of 5-6%.

After the rate hikes in 2022-2023, our variable mortgage peaked at 6.01% in mid-2023 and lingered there for a year. Ouch, wishing we took that fixed rate mortgage back in 2021.

2022-2023: Absorbing higher rates by making additional repayments

Just as we planned, we increased our lump sum mortgage payments to offset each interest rate hike that happened in 2022-2023. Every month, we would aim for an extra payment equivalent to the monthly interest differential between the prevailing interest rate and our initial 1.26% rate when we refinanced. This allowed us to keep our amortization schedule the same as before the interest rate hikes.

While we made these extra payments work, it’s not like we had unused cash lying around every month to bump up our payments. Any lump sum payments were redirected away from existing purposes, whether that be reducing our savings rate or cutting down on our day-to-day spending.

2024: Reducing lump sum payments as rates declined

As rates started coming down in mid-2024, we reduced our lump sum payments as the interest costs declined.

Normally, we would have directed the lump sum cash reductions towards our TFSAs or RRSPs. Since we were expecting a second baby, we diverted the cash towards our baby fund instead.

In 2025, while I am still on maternity leave with only Mr. LJ’s one income, we will use the lump sum reductions towards our ongoing monthly expenses. Once I go back to work (and if rates continue to stay low), we will accelerate our TFSA and RRSP savings again.

We will not be moving to a fixed rate mortgage

While the rates have come down on variable mortgages, fixed rate mortgages have remained flat. The rate gap between variable and fixed rate mortgages have narrowed. The markets are expecting further variable rate decreases, with limited impact on fixed rate mortgages.

We have weathered the tough parts of a variable mortgage already when rates peaked at ~6%. We did this while living off one income during maternity leave in 2023! With a narrowed rate gap, there is no good reason for us to move to a fixed rate mortgage right now. We’ll stick it out with variable and adjust our lump sum payments as needed.