Over the past couple of months, we’ve been anticipating central banks to raise interest rates. This would put pressure on household free cashflow, as interest rate costs would increase on consumer debt. Not surprisingly, Bank of Canada is raising alarm bells on the high levels of mortgage debt, which causes vulnerabilities in the Canadian economic system.

As one of the many Canadians who purchased a home in the 2020/2021 COVID years, I am fully aware of the high real estate prices (and resulting mortgage debt) that we signed up for. To make matters worse, just this past December, we refinanced our mortgage to a variable rate mortgage. We are taking these interest rate punches straight up in the face.

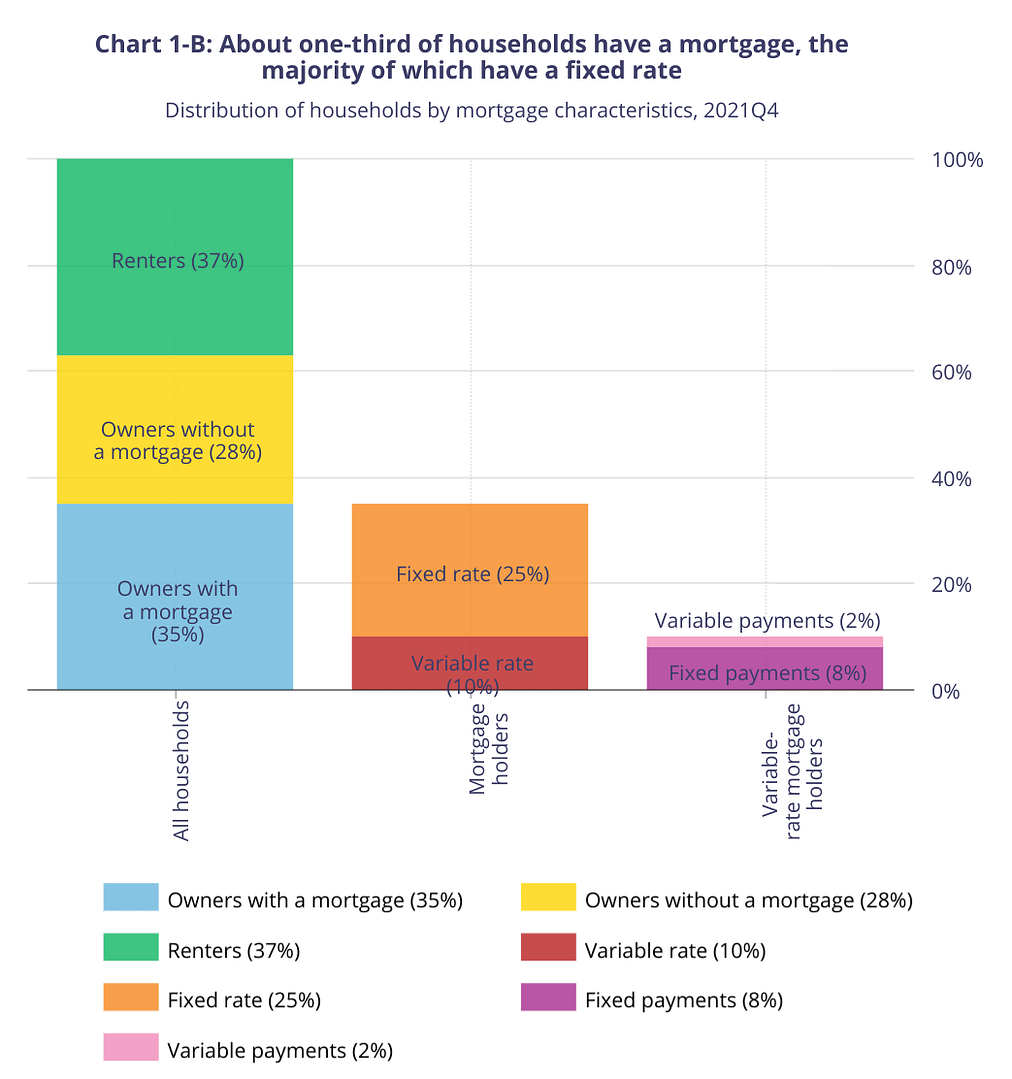

If you’re on a fixed rate, why does this matter?

About a third of Canadian households hold a mortgage, with 5 out of 7 holding fixed rate mortgages. While interest rate increases won’t impact these fixed rate holders during their mortgage term, costs will pop upon renewal. Bank of Canada estimates that monthly payments on fixed rate mortgages will pop +25%, while variable rate mortgages could jump +45% at renewal. Ouch, that’s painful.

So while fixed rate mortgage holders will temporarily win, the headwinds are coming at renewal. Why not prepare while you reap the benefits of low rates on your mortgage?

Does this mean you should repay the mortgage faster?

In a perfect world, we’d all have enough cash to pay for our needs & wants, save for retirement & children’s education, and repay our mortgages quickly. But life is messy and with inflation rising quickly, it’s taking more cash to buy the things we need.

In my asset location post about how to prioritize contributions, the lowest priority is contributing to “taxable investments or mortgage repayment”. So if cash is tight, repaying the mortgage faster is the least of your worries.

However, if you are fortunate enough to have maxed out your registered accounts that have preferential tax treatment, where should you put your extra cash? Is repaying the mortgage or investing in taxable accounts better?

After falling into the Google rabbit-hole, there are two common approaches.

1. Compare mortgage interest rate vs. after-tax investment return rate

Mortgage payments and interest are paid with after-tax dollars. So to quantify which option will have you mathematically ahead, you should compare:

- After-tax investment return: assume your portfolio returns 5% a year and your portfolio returns are taxed at 20%, your after-tax investment rate is 4%.

- Mortgage interest rate: fixed rate of 3% for the next 5 years

In this case, you are better off investing your cash at 4% after-tax than to repay a mortgage with 3% interest.

Sounds simple enough.

… except for a few complications …

- Fixed vs. variable rate: If you’re on a fixed rate mortgage, then this calculation is straight forward. However, if you are on a variable rate mortgage, the calculus becomes more complex. Since the interest rate could potentially fluctuate, it’s difficult to make a quantitative comparison.

- Changing rates of return on investments: There are years where the equity markets can be flat or declining. It can feel horrible to “not lock in a guaranteed return” by repaying your mortgage.

Instead of a rational, quantitative based approach, what about an emotional approach to answering the question?

2. Repay your mortgage because it feels great to be debt free

The emotional weight that’s lifted when debt repayments are no longer needed is an elating feeling. It’s psychological and emotional freedom. It provides so much flexibility, whether it means more cash flow every month to do other things or just the ability to quit a job you hate. There’s nothing wrong with that.

I found it interesting that another financial blogger said paying off his mortgage caused his drive to decrease. There was no longer the monthly need to pay towards the mortgage to keep a roof over his head. The desire to try hard at work to make more money falls away.

Unless you’re only a few years away from retirement, I think it’s important to have a bit of financial stress (in the form of a mortgage) to ensure your drive doesn’t disappear. If your drive falls too early before retirement, it could impact your earnings and savings potential from your career.

If you’re still uncertain, then why not do both?

Maybe you’re torn between following your quantitative brain or your emotional heart in investing vs repaying the mortgage. Why not do both? You can split some of your excess cash into a taxable investment account, and sprinkle a bit more against your mortgage.

Personal finance is personal and is meant to reflect the values most important to you. If you have the excess cash to be troubled by this “invest vs. repay” question, it’s a great dilemma to have. Whether you invest in a taxable account or repay your mortgage, you will still be better off than the average household.

Our plans are to repay mortgage to a certain point and then invest in taxable accounts

We still have some room in our TFSAs and RRSPs, so we don’t have any excess cash to have to make the invest-or-repay choice right now.

However, our plan was to increase our mortgage payments as if rates were 5%. Why would we want to do that?

1. Mortgage interest rate will likely be similar or higher than the after-tax investment returns

Firstly, equity market returns are expected to be lower than the past 10 years. My asset allocation is 42% US with remainder in global equities, which is estimated to generate ~5.5% before taxes. At a 50% taxable capital gains rate and an assumed 40% personal tax rate, I’d expect my portfolio to return ~4.4% after taxes.

Source: Vanguard, May 2022

In contrast, the interest rate on mortgages is expected to rise. Take a look at the historical 5-year fixed mortgage rates over the past 25 years in Canada:

Over the past 25 years, we’ve enjoyed extremely low rates as compared to the higher rates in 1980s and 1990s. While 5% isn’t a rate that we’ve seen in almost two decades, the inflationary concerns in 2022 is enough to potentially push us to that level within the year. I’d expect the banks to raise rates another 1.5% before the end of 2022. So, the interest rate on our mortgage will likely be similar or even higher than the after-tax returns of investments.

If I follow my quantitative brain, then it makes sense to repay the mortgage instead of investing.

2. Proactive living on less

Secondly, we plan to bump up our recurring payments to reflect a 5% rate to be used to managing our household cashflows at that level. In the event that rates become that high, we would have some practice living on lower cashflows. Call it “living on less”.

If those higher rates never materialize, great! We’ve put ourselves on a path to repay the mortgage faster, which is one of our financial independence goals. If those higher rates do materialize, we would have been living on less and there would be less painful changes to our lifestyle.

And if we’re lucky enough that we still have excess cash after making those mortgage payments? Then we can start investing in a taxable account under the spouse with the lower personal tax rate (current & projected). Hopefully we can get to this point in the next 2 years.