In the first post of the RRSP 101 series, it laid out the basics of the registered retirement savings plan.

After understanding the purpose and associated terminology, you should understand how the tax deferral works within an RRSP.

My brother followed traditional advice and contributed to his RRSP at the beginning of his career. He didn’t see as much benefit as he had envisioned because he didn’t understand how the tax deferral works with using the RRSP.

While it is usually never a bad idea to save towards retirement, you should understand where you are putting your money and what benefits each investment account provides. At the end of the day, no one will (or should) care more about your money than you do. So it’s worth spending some time understanding how the RRSP tax deferral works. This way, you can assess whether the RRSP makes sense for you.

Tax-deferred investment growth

The main benefit of the RRSP is that any contributions can be deducted to reduce your taxable income in a given year. This means that you won’t get taxed on the deduction amount and will likely receive a tax refund. If you reinvest the refund amount, you can use your refund to further growth your investment balance.

However, this tax-deferred investment growth only occurs if you reinvest the refund you receive. If you spend the money on a vacation or a renovation, then it becomes more like a taxable investment account with a higher tax burden.

Let’s use some examples to demonstrate.

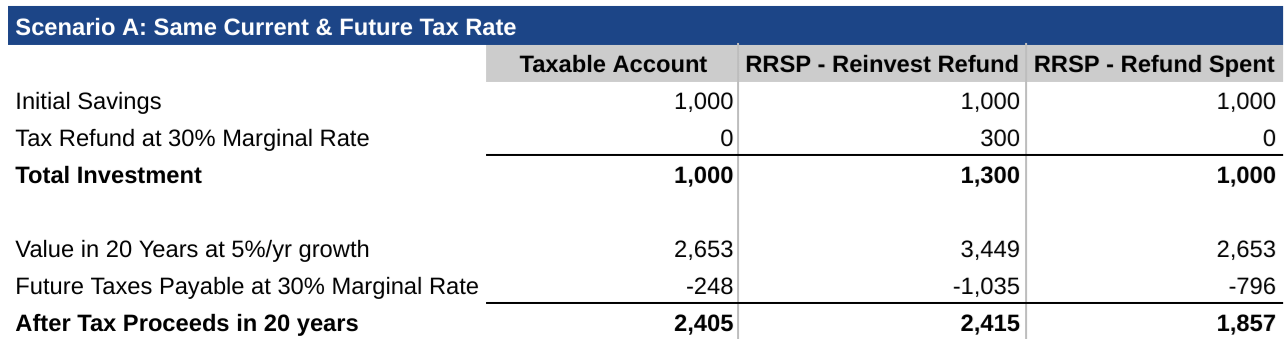

Scenario A: Reinvesting or Spending the RRSP Refund

In Scenario A, an individual has contributed $1,000 from their paycheques into either a taxable investment account or an RRSP. They invest the cash in equities. Assuming the marginal tax rate is the same when the RRSP deduction is taken today and when the withdrawals happen in the future, the after-tax proceeds is relatively the same.

However, that is only true if the tax refund is reinvested back into the RRSP. If the individual spends that money, the tax deferral benefit is completely lost. In this case, the RRSP where a refund is spent generates lower after-tax proceeds than the taxable account.

Why is that? It’s because of how RRSPs are taxed upon withdrawal. The full amount of an RRSP withdrawal is taxed as income, where the withdrawal amount could include a mix of contributions and investment gains.

In contrast, tax is paid on the investment gains within taxable accounts. In this example, the individual had invested in equities. Only 50% of any capital gains are considered as taxable. The original investment amount is not subject to tax.

This difference exists because the Canadian tax system seeks balance and makes things fair:

- In RRSPs, contributions that are deducted generate a full refund at the individual’s marginal tax rate. Since the contribution was never taxed, it is fair for the amount to become taxable upon withdrawal

- In a taxable account, the contribution or original investment amount is from an individual’s after-tax income. Since the original investment amount was already taxed, it is fair for the amount to not be taxable upon a sale of your investment

Let’s go back to the Scenario A example. If the taxable account and the RRSP (refund reinvested) account generates roughly the same after-tax proceeds, then why invest in the RRSP at all?

The power of the RRSP is all in the difference in current and future tax rates.

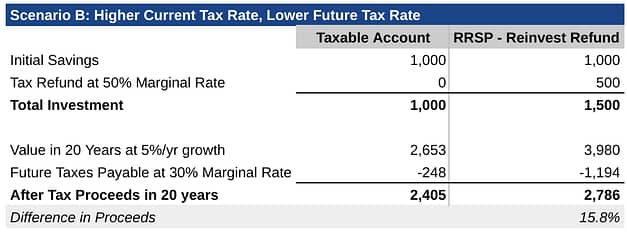

Scenario B: Higher Current Tax Rate vs. Lower Future Tax Rate

In Scenario B, the individual also contributes $1,000 from their paycheques. Since they are in their peak earning years, they are currently being taxed at a high 50% marginal tax rate. If they deduct the $1,000 against their taxable income, it would generate a refund of $500 which they could reinvest in their RRSP.

Fast forward 20 years, the individual has retired and withdraws from their RRSP at a (comparatively) lower marginal rate of 30%. Compared to investing in a taxable account, the RRSP leads to almost 16% higher (or $380 more) in after-tax proceeds.

The tax-deferral power of the RRSP is maximized when your tax rate is lower when you withdraw in the future. The ~$380 of higher proceeds is largely attributed to the differences in taxes payable on the total investment of $1,500.

If the marginal tax rates were the same in the future, the $1,500 would be subject to 50% tax, or $750 in taxes payable. Instead, the investment amount is only subject to 30% tax, or $450 in taxes payable. This leads to $300 more in after-tax proceeds.

It makes sense that marginal tax rates in the retirement years are lower than peak income earning years. But this isn’t always the case.

Scenario C: Lower Current Tax Rate vs. Higher Future Tax Rate

In Scenario C, the individual is in a low tax bracket of 15%. This could be someone at the start of their careers or someone who only had partial earnings in the year. If they deduct the $1,000 against their taxable income, it would generate a comparatively smaller refund of $150.

In another 20 years, the individual is now in a higher tax bracket of 30%. This could be due to very high growth in their investment accounts. Or someone who is semi-retired with employment income and RRSP withdrawals. It could also be someone who had to withdraw a large amount from RRSPs in a given year for unforeseen circumstances. There are many other scenarios that could cause a higher tax bracket in the future.

If an individual has a higher future tax rate, this will lead to lower after-tax proceeds than if they invested in their taxable account. This shouldn’t be surprising, as the aforementioned tax deferral power of the RRSP is flipped 180. It becomes a tax burden to the individual instead.

Save money by being realistic about your future tax rate

While it’s next to impossible to accurately predict where your marginal tax rate decades into the future, there are a few considerations that can help:

- Consider the earnings potential of your career: perhaps you’re in an industry or a career path where your future earnings growth is predictable. If so, it would be best to delay any RRSP deduction until you reach those high taxable income years.

- Even if your career doesn’t have a defined path, be honest with yourself. Are you the type of person to want to climb the career ladder? Are you one to negotiate salaries? Or switch jobs for better pay or career progression? If yes, then bet on yourself and your earnings potential. Save the RRSP deduction until later.

- Stop contributing if your RRSP has a sizeable balance: the main benefit of RRSP is savings based on tax rate difference between today and the future. If you have been a diligent saver or have outsized gains within your portfolio, the amount in your RRSP could be high. (Maybe you returned 10x or 20x on some your investments!) It’s best to stop contributing to your RRSP, as your taxable income upon RRSP withdrawal could be higher than your income earning years.

- The table below shows the annual amounts you can withdraw from your RRSPs. It shows different opening balances at the start of withdrawal and the number of years to withdraw.

- Example – Continue to contribute: You’re planning to retire at 50 and expect a 40 year withdrawal. During your working years, you averaged $70K taxable income. If you have a $200K RRSP balance, you could withdraw $11,656 annually (assuming a 5% growth rate per year). Unless you have a lot of other taxable income to get you to above $70K in your retirement years, you could probably continue contributing to your RRSPs.

- Example – Stop contributions: Instead of a $200K balance, your RRSP account has grown significantly to $900K. This means you could withdraw $52,450 annually. If you have other taxable income like CPP payouts or rental income, it could easily push you above the $70K taxable income amount*. This means that the taxable income in your retirement years is higher than your income earnings years. This will likely result in you paying more tax in retirement than the tax break benefit in your earning years.

(*While taxable income brackets and associated tax rates are likely to increase over time, I have kept it flat for simplicity)

The tax deferral benefits from the RRSP requires an understanding of our tax system and some pre-planning. It’s a bit complex, but the tax savings could be substantial. It’s definitely worth investing a few hours to understand how the tax deferral benefit works in RRSP accounts.