Rebalancing a portfolio means buying or selling different assets to get back to your target allocations. In a fluctuating market, the outperforming assets grow to become a greater proportion of your portfolio. So rebalancing usually means selling the winners and buying more into the laggards.

Rebalancing minimizes risk but also reduces returns

When an asset class outperforms, it’s unknown whether it will keep increasing or will decrease in the future. It’s tempting to believe that prices will continue rising forever, but we know that the market doesn’t just move in a straight line upwards.

This Vauguard research paper shows the returns and risk profile of rebalancing and not rebalancing a 50% equities and 50% bond portfolio. For the rebalanced portfolio, the return is lower, but the risk profile is significantly lower than the never-rebalanced portfolio.

The lower return makes sense, because you are selling the outperforming assets and buying the underperforming assets. The lower voatility also makes sense, because outperforming assets can’t continue rising forever. The risk of the asset decreasing becomes greater.

How do you rebalance?

If you are only invested in Target Date Funds or an all-in-one asset allocation ETF such as VEQT or XEQT, then you don’t have to do anything. The fund manager will rebalance for you (and all the other investors in those funds).

If you have constructed your own portfolio or if you have multiple portfolios that have different allocations, you will need to track the current portfolio allocation and your desired target allocation. You can then calculate the difference between your current and your target to understand which asset class and how much to rebalance.

If you’re in the asset accumulation phase, you can rebalance by investing your recurring contributions. Maybe you contribute every paycheque, so you can buy into the underperforming assets to rebalance.

If you’re in the decumulation phase or your portfolio has grown large enough that your contributions can’t fully rebalance your portfolio, you may have to sell some winners to rebalance back into the laggards.

If it’s in a taxable account, there could be tax implications that could change the rebalancing approach. Also consider the impact of any trading costs, which could further cut into your expected returns of rebalancing.

Rebalancing can feel wrong

In a down market, rebalancing can feel wrong. It requires adding more into underperforming segments. It’s going against the grain and where the broader market is winning. Buying into something that has lost value is hard. Sticking to asset allocation targets is hard.

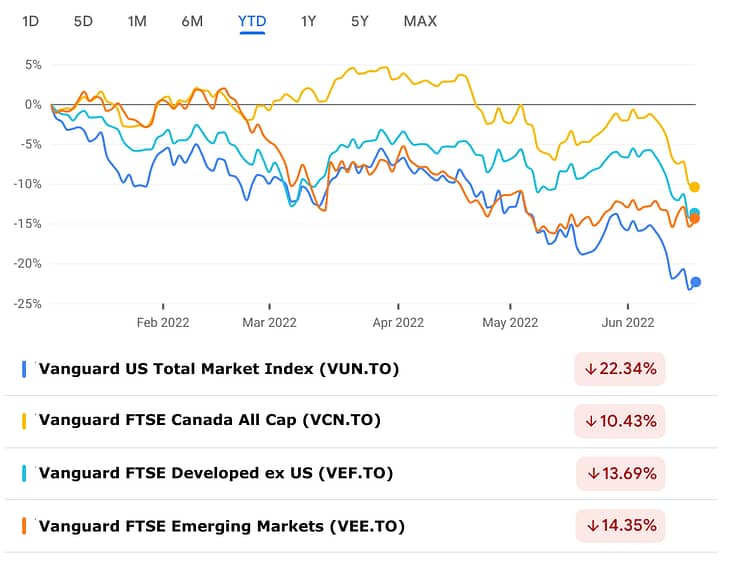

For our overall portfolio, we set asset allocation targets by geographical equity type. Recently, we had a bit of cash to deploy, so I updated our portfolio tracking sheet to see which ETF the money should be invested in.

I was surprised to see that we were underweighted in both US and Emerging Markets equities. After thinking about it for a few minutes, it makes absolute sense. To date in 2022, US and Emerging Market equities declined more than Canadian equities.

Although the portfolio tracker showed I needed to deploy cash into US and Emerging Market equities, I was reluctant to do it. It just felt wrong to put more cash into a declining sector.

Since I am in the asset accumulation phase, I was going to invest that cash regardless. Despite my reluctance, I followed through on adding cash into US and Emerging Markets to return our portfolio back to the target allocation.

Rebalancing annually or quarterly is sufficient

With market prices moving every minute, it’s impossible to be 100% aligned to your target allocation. How often should you rebalance?

The Vanguard research shows that rebalancing monthly, quarterly and annually all have a similar risk/return profile. Given that, it’s sufficient to rebalance annually or quarterly depending on your personal preference.

For our portfolios, we rebalance whenever we invest our biweekly contributions. This means we buy into our under-allocated segments and stop buying into over-allocated areas. However, if our contributions aren’t sufficient to put us back to our targets, we do not actively sell our positions to rebalance every month. We would do so on an annual or semi-annual basis.