With the world gripped in uncertainty of war and concerns of inflation (and stagflation), it’s easy to get pulled into the doom and gloom. It’s even easier to be compelled to “do something” to protect your portfolio.

Before the world descends into further chaos, it’s important to write out the plan. Write out the investment principles that will guide your decisions in times of uncertainty.

Just like how airlines show you the pre-flight safety videos in case of emergency, it’s best to figure out your investment principles before you hit turbulent markets. (I am not suggesting that markets will crash, but you should always be mentally prepared that it’s a possibility.)

I spend a lot of time thinking about how to invest the money that we laboriously saved. It’s a two-fold reason: (1) make sure we are returning returns competitive with the average market, and (2) not make emotional and irrational mistakes in the bumpy stock market ride.

Here’s our investment principles that guide us through both choppy and calm markets.

Principle 1: Always be buying

With a long term (20+ years) horizon, we need to benefit from the expected increases in the equities market. We don’t try to time the market, because I can’t tell if day-to-day markets are trending up, trending down, peaked or bottomed out. If I could predict it, I would just daytrade everyday and make a living on that instead!

To free up mindspace, we consistently buy into the markets when our biweekly contributions hit the investment accounts. When prices trend downwards, we are excited to buy. When prices trend upwards, we “feel” like we missed out on lower prices but we still buy regardless.

Given our compensation packages with our employers and our tax refunds, we end up with lumpy inflows of cash around March to May every year. These could be as high as 5-figure balances. While we know that history would show lump sum investing beats out dollar cost averaging the balance about two-thirds of the time, we usually split our lump sum and invest that over a 3 month period.

Principle 2: Don’t panic sell

Since we are in it for the long game, we shouldn’t be concerned with the short or medium term market fluctuations. We have a healthy emergency fund and don’t need to use our investment portfolio to fund our living expenses.

The worst decision is selling in a down market. First, you crystallize and lock in your losses. Second, you end up holding cash for too long because you don’t know whether markets have bottomed. This means you will most likely miss the inevitable upswing when the markets return.

If we can’t live through the volatility, it means we should adjust our asset allocation to match a lower risk appetite. This is connected with the next principle.

Principle 3: Invest in diversified, low-fee ETFs

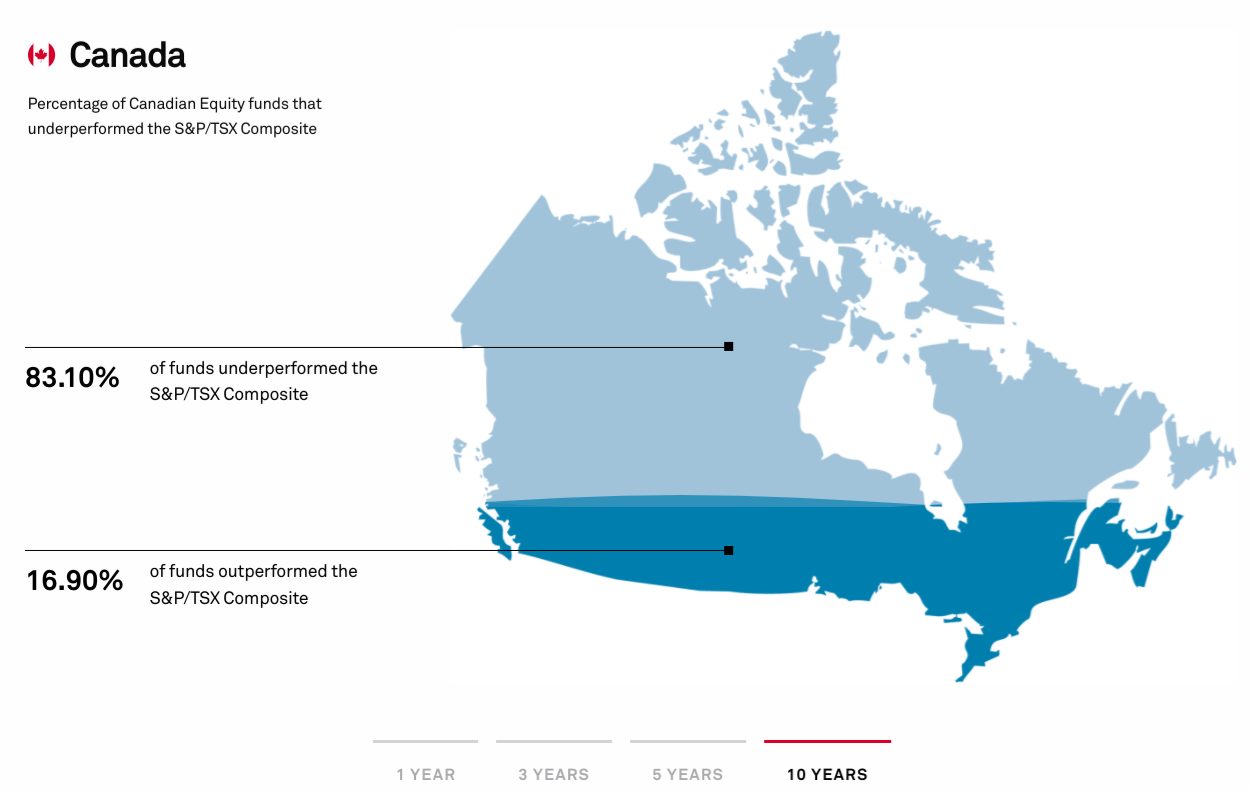

I’m not good at picking stocks. My track record of mistakes has been atrocious.

Studies show that a majority of active investors are not going to beat the market. I have enough humility to recognize that I am not better or smarter than the average active investor.

To make sure we don’t underperform to the market, we hold diversified ETFs for 95%+ of our accounts. Why don’t we do that for 100% of it? Well, just to satisfy my desire to support and invest in companies I believe in.

So we leave a small sliver of 5% to invest in equities of mature companies in North America. We’re not buying into penny stocks and SPACs, so I don’t expect these companies to implode to zero and wipe out 5% of our investments.

Principle 4: Simplicity over complexity

Simplicity is easier to follow, usually lower fees, and less mentally taxing than complexity. This includes:

- Automating contributions from our chequing account into our investment accounts

- Investing in all-in-one asset allocation ETFs instead of multiple ETFs

- Avoiding complex instruments, like options and private equity or venture capital funds

- Minimizing the number of investment accounts to manage. At one point, I had 3-4 separate TFSAs! It was too difficult to track contributions and asset allocation

Principle 5: Maintain similar investment balances across the spouses’ accounts

This is especially important in RRSPs and taxable investment accounts where a tax bill will eventually have to be paid. If one spouse has a large taxable account balance and the other has a small one, this may cause a higher overall tax bill to be paid. Planning ahead ensures we don’t run into issues where one spouses’ accounts are significantly larger than the other spouses’ accounts in the future.

(We are indifferent about the balances in our TFSAs, as there are no tax implications upon withdrawal)

You might think “well there are RRSP pension income splitting rules, there’s no need to plan for this!” Regulation changes happen, government parties change over time. Who knows if RRSP income splitting will still be accessible in the future? By proactively balancing out investment balances now, it prevents future headaches.

Principle 6: Target asset allocation maintained across all accounts

We maintain a similar asset allocation across each of our investment accounts. This means that our geographic and equity/bond allocations are basically the same across everyone’s TFSA, RRSP or and taxable accounts.

The reason is because Principle #5 and maintaining similar balances. While we can control the contributions going into the accounts, we have to manage the growth rate of the accounts to make sure we end up with similar account balances after 20-30 years of compounded growth.

You can find more about our target allocation in our financial plan.

Principle 7: Max out tax-advantaged accounts before investing in taxable accounts

I fell into the trap of “putting investments into the most tax efficient accounts.” This meant I put Canadian dividend-paying stocks into a taxable account even though I had significant room in my TFSA. It was nonsensical to pay personal taxes on the dividends when it could be sheltered in the TFSA.

For simplicity, our goal is to max out our TFSA and RRSP room.

There are some edge cases where it’s not desirable to invest in tax-advantaged accounts. Maybe our RRSP balances have ballooned to a multi-million dollar amount; then adding more to that RRSP balance would have lead to higher taxes on withdrawal.

Develop your own investment principles

Many of these investment principles can be broadly applied to the average investor. As with everything in personal finance, it is highly personal to your own situation. There may be some tax-specific or family-specific considerations to build into your own principles.

Principles are meant to guide us when the journey gets rough. Make sure you have yours in place before making investing decisions you might regret.