When I first started investing, I had never heard of the concept of “Asset Allocation”. I had always assumed investing meant buying individual stocks that matched with growing trends.

If the news said “oil will go up”, that meant I bought oil stocks! If my family and friends gave me stock tips, those are the ones to buy!

Needless to say, I learned the hard way that that’s not the right way to invest. My investments weren’t made according to any plan other than hearsay and rumours.

Here’s where “asset allocation” would have helped my investment decision making.

Asset allocation is like the blueprint before you build a house. To invest without knowing what your asset allocation is like building your house without knowing the layout of all the rooms in your house. Without a plan, you’re probably going to waste time, spend more than you expected and the final product might not meet your needs.

What is Asset Allocation?

Asset allocation is identifying the right mix of stocks, bonds and other assets that balances (1) achieving your investment targets and (2) letting you sleep well at night.

Achieving your investment targets

Setting an inappropriate asset allocation mix means your portfolio could lead to you missing your desired investment dollars in the time horizon that you need it.

For example, you could put all your retirement money into a high-interest savings account. Based on today’s savings account interest rates generally below 1% at the big banks, a $1,000 investment would only grow to $1,644 in 50 years! Your money wouldn’t even double. With inflation generally around 2%, you would lose purchasing power every year despite earning 1% interest. This would not bode well for your retirement.

Letting you sleep well at night

You could also set an asset allocation that, on paper, lets you achieve your investment targets.

For example, you could put all your money into Bitcoin, which has an annualized average return of 200%+. With just a $1,000 investment into BTC, you could have $2 million in just 7 years!

While the math works out on paper, we know historical returns are not guaranteed into the future. We also know that Bitcoin (and cryptocurrencies) are a very volatile asset, meaning there are large price swings. Since 2020, there have been multiple -50% crashes in just a single month.

Would you be able to sleep at night knowing your savings were halved in just a month? Would you have cashed out and put everything into your chequing account? Your reaction to these is called your level of “risk tolerance”.

Despite (potentially) meeting your return targets, your asset allocation should meet your level of risk tolerance. If the stress of holding highly volatile and risky assets gets to you, then you have a low risk tolerance. If you are able to handle big upward and downward swings in price without losing much sleep, then you have a high risk tolerance.

By crafting an asset allocation that meets your level of risk tolerance, you are more likely to stay invested during the inevitable market swings. If you choose an asset allocation that’s too aggressive for you, you are more likely to sell in a market crash, hold onto cash for too long and miss any price appreciation when it happens.

Early in my “investing career”, I made improper asset allocation decisions. It led to some late night angst and financial underperformance. But the best way to learn is to make mistakes, so I’m glad I made them early on.

Why does asset allocation matter?

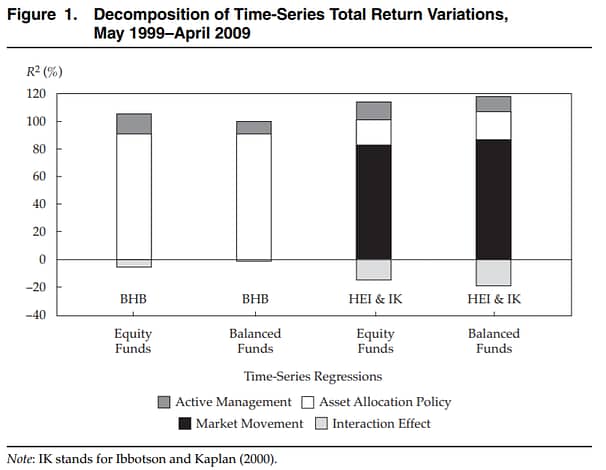

The findings from the study “The Equal Importance of Asset Allocation and Active Management”[1]James X. Xiong, Roger G. Ibbotson, Thomas M. Idzorek & Peng Chen (2010)The Equal Importance of Asset Allocation and Active Management, Financial Analysts Journal, 66:2, 22-30, DOI: … Continue reading found that:

About three-quarters of a typical fund’s variation in time-series returns comes from general market movement, with the remaining quarter driven roughly equally by the asset allocation policy and active management.

This means ~75% of the portfolio returns is based on the general upswings and downswings of the stock market movements. By staying invested in the market, the investor will benefit from the “general tide lifting all boats” phenomenon.

The remaining ~25% is driven by investor choices in both asset allocation and active management. Active management requires a lot of ongoing time, effort and energy that may not translate to outperformance by the individual investor. However, asset allocation is a lower-effort choice that the average investor can make to drive returns.

Equities vs. Bonds – Risk, Return & Volatility

Equities have historically offered investors a higher return on investment compared to bonds. Risky assets, like equities, need to compensate investors with the potential for a higher return. Compared to bonds, equity pricing and returns are also more volatile, with a wide variation or range of investment returns.

The best way to think about equities vs. bonds is “high risk, high reward”. Equities offer “higher risk, higher reward”, whereas bonds offer “lower risk, lower reward”.

In asset allocation, it’s determining the appropriate mix of equities, bonds and other assets that offers the risk-adjusted returns that achieves your financial goals and lets you sleep at night.

Traditional Equity/Bond Allocation Recommendations

Typical asset allocation advice largely falls in one of these buckets:

1. 110 (or 100) less your current age = % allocation to equities

Example: If you were 40 years old, you should allocate 70% to equities (110 less 40) and remaining 30% to bonds

This recommendation assumes you will follow a traditional 65 year old retirement age. For those seeking financial independence earlier, this probably won’t get you there quick enough.

2. 60/40 portfolio

Example: regardless of your age, set 60% in equities and 40% in bond

This recommendation is too generic and doesn’t take into account any time-based metric, like your age or number of years until retirement.

These rules-of-thumb are easy to remember and is a good first step for the average person. If you want to stop here, you will be significantly better off most of the population.

However, as the CEO of your retirement, why should you use rules-of-thumb when asset allocation is such a critical driver of returns?

As a prudent CEO, it’s your job to know more and decide whether to set an asset allocation that differs from traditional recommendations. No one will care more about your retirement than yourself.

Historical Returns of Portfolios at Different Equity/Bond Allocations

In any given year, different equity markets across the world have different levels of returns and volatility.

From 2007 to 2021, these are the annual returns for major equity and bond asset classes:

Special thanks to the source data from Novel Investor

While equity markets are oftentimes directionally similar, there are times when the results differ. Using 2021 as an example, Canada, US and International stocks saw positive returns, whereas Emerging Markets declined.

In comparison, you can see bonds (grey box in chart above) generate more steady returns. It’s less volatile than the “high high’s and low low’s” of the equity markets.

Bond returns are less correlated with the equity markets. While there are times bonds follow the directional return of stocks, there are just as many times where bonds diverge from stocks.

While understanding volatility and returns in a given year is useful, you are likely not just investing for just one year. If you are investing for retirement, you should zoom out to see longer periods to understand how it applies to your portfolio.

Special thanks to the source data from Novel Investor

Markets have been reliable in generating positive returns over long periods of time. While volatility could see values been chopped in half in any given year, markets are positive over time.

If markets just go up, why do we need asset allocation? While returns can meet your objective, asset allocation also allows you sleep at night.

With this basic understanding, let’s look at how combining a mix of equities and bonds at different levels leads to differing returns and volatility .

Hypothetical US Equity & Bond Portfolios

Let’s assume an initial investment of $10,000 is made at the start of 2007. The $10,000 will be invested only in US Large Caps and US High Grade Bonds. Here’s how the investment would have fared at each 20% increment of US Large Caps & High Grade Bonds.

Portfolio rebalanced annually back to target equity/bond % allocation targets on Dec 31.

No fees or transaction costs.

As expected, a 100% US equity portfolio underperformed all other allocations during the Great Financial Crisis in 2008-2009. A 100% US bond portfolio outperformed all others from 2007 through to 2012.

By around 2013, the equities returns exceeded bond returns and all allocation portfolios had relatively similar values.

Since 2013, the equity market returns have been on fire, especially from 2018 onwards.

The following chart shows the highest, lowest and average annual returns at each 20% increment of US Large Cap and US High Grade Bonds:

While any one year can have large positive and negative return swings, a longer term horizon (say a 15-year time frame in 2007-21) is largely positive.

(Yes, you could argue that using 2007 to 2021 is cherry-picking dates and returns. While I won’t delve into the calculations, one of my favourite financial blogger has a number of comprehensive analysis that looks at more historical data. The conclusion remains the same: the longer you zoom out your time horizon, the more likely you are to achieve positive returns.)

What equity/bond allocation should you pick?

Any equity/bond allocation you pick should let you hit your financial targets and let you sleep well at night. If you’re looking for more specific recommendation on an equity/bond allocation, read on!

Instead of the traditional “age based” formula, I recommend basing the allocation decision on when you need the funds. As an example, you could be 40 years old today and want to retire by 55. This means you need the funds in 15 years.

Why base it on that? In any given year, asset returns are volatile and could be very high or very low. If you need the money in the short term, you don’t want that risk. The longer you zoom out, the more likely your portfolio will have positive returns.

This recommendation is what I follow. I have a high risk tolerance and am unlikely to sell my positions in downturns. I believe in the underlying upward momentum in equity markets over the long term. So I don’t really worry about the daily / monthly / annual fluctuations.

| Time Horizon | Equity % | Bond % |

| 5 years | 20% | 80% |

| 10 Years | 60% | 40% |

| 15 Years | 80% | 20% |

| 20+ Years | 100% | 0% |

As always, personal finance is highly personal. What works for me might not work for you. So consider what equity / bond allocation makes the most sense to let you reach your goals and sleep well.

Now that you’ve figured out how much to allocate to equity and bonds, you need to figure out what proportion should be allocated to each country.

In an upcoming asset allocation post, I will walk through how to allocate amongst your home country vs. USA vs. international (developed and emerging).

References

| ↑1 | James X. Xiong, Roger G. Ibbotson, Thomas M. Idzorek & Peng Chen (2010) The Equal Importance of Asset Allocation and Active Management, Financial Analysts Journal, 66:2, 22-30, DOI: 10.2469/faj.v66.n2.7 |

|---|